|

- UID

- 12226

- 帖子

- 6753

- 精华

- 10

- 性别

- 男

- 来自

- 上海

- 注册时间

- 2008-4-12

访问个人博客

|

楼主

发表于 2014-4-17 07:25

发表于 2014-4-17 07:25

| 只看该作者

[转帖] 【2014.3.8】Business in emerging markets 新兴市场中的企业

http://www.ecocn.org/thread-197671-1-1.html

Business in emerging markets

新兴市场中的企业

Emerge, splurge, purge

开始起步,大量投资,清洗业务

Western firms have piled into emerging markets in the past 20 years. Now comes the reckoning

过去20年间西方企业不断涌入新兴市场国家。现在到了进行总结的时刻了。

Mar 8th 2014 | From the print edition

Phone users smile, shareholders weep

手机用户一笑,股东就哭

VODAFONE’S latest figures appear at first glance to vindicate the most powerful management idea of the past two decades: that firms should expand in fast-growing emerging economies. Sales at the mobile-phone company fell in the rich world while those in the developing world rose smartly. Corporate strategy is usually a contentious subject: there are fierce debates about how big, diversified and financially leveraged firms should be. But geography has seduced everyone. Vodafone is one of countless Western companies that have bet on the developing world.

Look closer, however, and those figures contradict accepted wisdom. At market exchange rates Vodafone’s sales in the emerging world fell, reflecting the widespread currency depreciations in mid-2013, when America’s Federal Reserve signalled it would taper its bond purchases. This drag may linger: in January the lira and rand tumbled in Turkey and South Africa, two biggish markets for Vodafone. On longer-term measures things look cloudy, too. Over a decade Vodafone has invested more than $25 billion in Turkey and India. These operations made a paltry 1% return on capital last year. Vodafone has created a lot of value for its shareholders—but through its American investments, which it has sold to Verizon for a stonking price.

乍看之下,沃达丰的最新数据可以证明过去20年来最有效的管理思路的正确性:那就是企业应该向发展迅速的新兴市场国家扩展。移动电话企业在发达国家的销售额减少,而在发展中国家的销售额却迅速增加。公司的发展战略通常是一个容易引起争论的话题:关于怎样的企业才算是业务多样化、有资金优势的大企业存在着激烈的争论。但是地理因素诱惑了所有人。达沃丰是众多将赌注压在发展中国家的企业之一。然而,仔细观察会发现这些数据有悖于普遍接受的观念。以市场汇率计算,沃达丰在新兴市场国家的销售额是下降的,这反映出2013年中期货币普遍贬值的现象,在同一时间美联储表示会减少购买债券。这种困境或许会持续下去:一月份土耳其里拉和南非兰特急剧贬值,而这两个国家也是沃达丰最大的两个市场。长期看形势仍然不容乐观。过去十年间沃达丰在土耳其和印度的投资总额超过250亿美元。而去年这些投入的资本收益率仅为1%。沃达丰为股东创造了极大的利益,但是是通过其美国投资部分,这部分投资已以高价卖给了威瑞森电信。

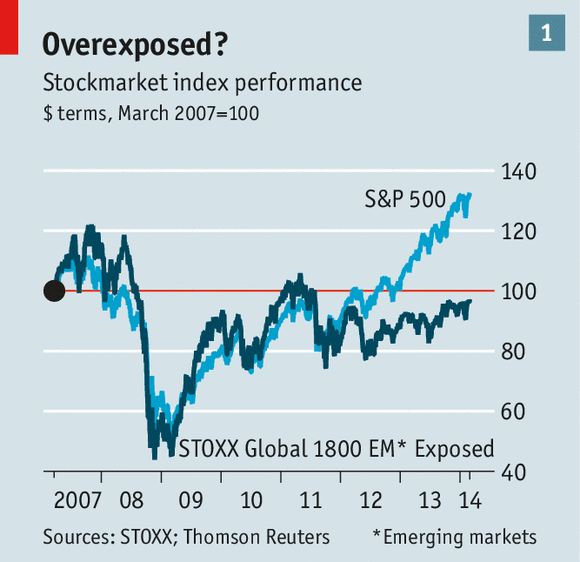

This year Western firms’ giant bet on the emerging world will come under more scrutiny. Most multinationals are far more profitable in emerging markets than Vodafone. American firms made a 12% return on equity in 2012, roughly in line with their global average. But having grown fast, profits are now falling in dollar terms. There has been a long bout of share-price underperformance as investors have lost their euphoria. An index run by Stoxx, a data firm, of Western firms with high emerging-market exposures has lagged the broader S&P 500 index by about 40% over three years (see chart 1). And the recovery in the rich world will mean there will be more competition for resources within firms. This year Western firms’ giant bet on the emerging world will come under more scrutiny. Most multinationals are far more profitable in emerging markets than Vodafone. American firms made a 12% return on equity in 2012, roughly in line with their global average. But having grown fast, profits are now falling in dollar terms. There has been a long bout of share-price underperformance as investors have lost their euphoria. An index run by Stoxx, a data firm, of Western firms with high emerging-market exposures has lagged the broader S&P 500 index by about 40% over three years (see chart 1). And the recovery in the rich world will mean there will be more competition for resources within firms.

今年西方企业在将赌注压在新兴市场国家的时候会进行更细致的调查研究。大多数跨国公司在新兴市场国家的利润比达沃丰的高得多。美国企业2012年的资本收益率是12%,基本与国际平均水平一致。但是经历利润快速增长后,以美元来计算,现在利润是在减少的。股票价格走低已经持续了很长一段时间,投资者们也不像一开始那么兴奋了。根据斯托克数据公司提供的数据,在过去三年间那些在新兴市场国家业务多的企业的指数大约已经落后于更广的标准普尔500指数的40%(见表1)。而发达国家经济不断复苏意味着企业内部的资源竞争会更加激烈。

All this will bring strategic questions into sharp relief. Divisional chiefs from Brazil or Asia will no longer get a blank cheque from their boards. Although the average company has prospered, there have been disasters; plenty of firms and some whole industries need a rethink. The emerging-market rush may end up like a giant version of the first internet boom 15 years ago. The broad thrust was right but some big mistakes were made.

所有这些会使关于发展战略的问题告一段落。巴西或者亚洲的区域主管不会从董事会那里得到空头支票了。虽然平均说来企业都得到发展,但是也有发展地极其糟糕的;许多企业甚至某些产业整体都需要重新作出思考。对新兴市场的追捧很可能最后会成为15年前互联网企业首次膨胀的巨型翻版。大规模涌入新兴市场并没有错但还是犯了一些重大错误。

The companies suffering a slowdown in profits come in three buckets. Consumer firms including Coca-Cola, Nestlé, Unilever and Procter & Gamble have suffered a gentle weakening in demand and a currency drag. Most are still upbeat about the long term, says Andrew Wood of Sanford C. Bernstein, an analysis firm.

利润下降的企业分为三类。包括可口可乐、雀巢、联合利华以及保洁公司在内的消费品公司都经历了需求略降、货币拖后腿的局面。Sanford C. Bernstein分析公司的安德鲁伍德(Andrew Wood)表示从长期看大多数企业的发展形势仍是乐观的。

Companies in the second bucket face a sharper slowdown. They are in cyclical and capital-intensive industries. Fiat Chrysler’s profits in Latin America, a vital cash cow, halved in 2013. This week Volkswagen and Renault joined the ranks of Western carmakers warning of weak emerging-market sales. Last month Peugeot wrote off $1.6 billion of assets, mainly in Russia and Latin America. Emerging-market sales have fallen at Cisco, a technology firm; its boss, John Chambers, reckons it is “the canary in the coal mine”. Industrial giants such as ABB and Alstom have seen orders falter for infrastructure projects, for example the building of power stations, says Andreas Willi of J.P. Morgan.

第二类企业的利润跌幅更大。它们属于周期性企业和资本密集型企业。2013年克莱斯勒公司在拉丁美洲的利润减半,而拉丁美洲是其主要的利润来源。本周大众公司和雷诺公司也加入了面临新兴市场销售额下降预警的诸多西方汽车制造公司的行列中。上个月标致公司冲销了16亿美元的资本,主要是在俄罗斯和美洲。思科公司在新兴市场国家的销售额也下降了,老板约翰钱伯斯(John Chambers)认为这是”金丝雀掉进了煤矿里“。据J.P.摩根公司的安德鲁威力(Andrew Willi),像ABB和阿尔斯通这样的工业巨头也面临着诸如发电站建设等基础设施工程订单减少的局面。

Those firms with mismatches—costs or debts in firm currencies but sales in depreciating ones—face a nasty squeeze. Margins in emerging markets have halved at Electrolux, which makes fridges and other appliances. Codere, a Spanish firm with an empire of gaming and betting shops in Latin America paid for with debts in euros, is now on life support and restructuring its balance-sheet.

那些成本和债务以企业所在国货币计算而销售额以贬值货币计算的企业的状况更加糟糕。制造冰箱和其它电器的伊莱克斯公司在新兴市场的利润已经减半。Codere是一家西班牙企业,在拉丁美洲拥有巨大的游戏和赌博产业,以欧元偿还债务,现在却处于仅仅能维持公司正常运转的状态,并在调整自己的资产负债表。

In the third bucket are firms with idiosyncratic problems. China’s war on graft has hurt luxury-product makers that have grown fat by selling bling to the Middle Kingdom. Sales at Rémy Cointreau, which makes cognac that Communist Party big-shots quaff, fell by a fifth in the quarter to December, compared with the previous year. Russia’s once-frothy beer market is shrinking as the country conducts one of its periodic crackdowns on alcoholism.

第三类企业面临的问题各不相同。中国对腐败宣战导致奢侈品制造商蒙受巨大损失,这些奢侈品制造商正是通过向这个中央帝国卖奢侈品才壮大起来。人头马公司制造的白兰地中共的大人物都喜欢喝,其在第四个季度的销售额与去年相比,下降了五分之一。而俄罗斯的泡沫啤酒市场的销售额也因为该国周期性整治酗酒现象而缩水。

All this may be breezily dismissed as short-term turbulence. But emerging-market wobbles can have a profound impact on corporate strategy. After the 1997-98 Asian crisis many multinationals tilted back towards the rich world. Citigroup and HSBC, two big banks, played down their Asian heritages and spent the next decade building subprime and investment-banking operations in America. Unilever’s operating profits fell in 1997. It felt obliged to tell shareholders that the rich world was its “backbone” and by 2000 it too had made a huge American acquisition, of Bestfoods.

所有这些都可视为短期不稳定现象而不必给予太多关注。但是新兴市场的不稳定性可能会对企业的发展战略产生巨大影响。1997-98年亚洲金融危机后许多跨过公司撤回发达国家。花旗银行和汇丰银行缩减其在亚洲的业务,用接下来的十年时间在美国建立起次级抵押贷款和投资银行业务。联合利华1997年的营业利润下降,这使其认为有义务告知股东们发达国家才是企业的”支柱“,2000年它大型收购了美国的贝斯特食品公司。

Rising exposure

业务不断扩大

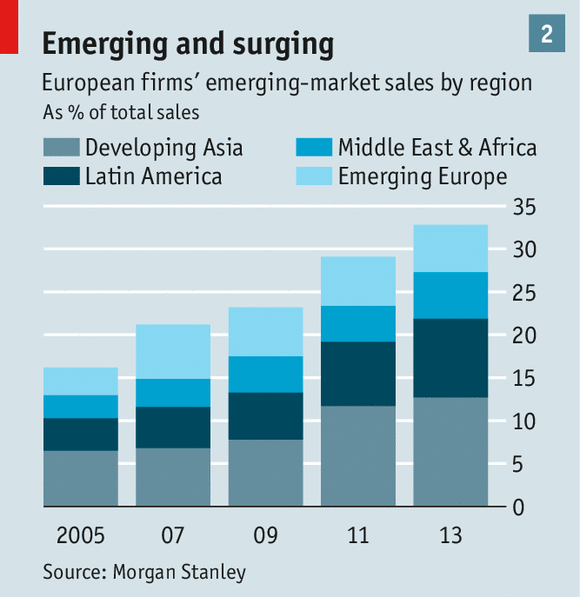

The emerging world’s troubles are not as bad as in 1997-98. But the exposure of rich-world firms is far higher than then (see chart 2). Big European firms make one-third of their sales in the developing world, almost triple the level in 1997, reckons Graham Secker of Morgan Stanley. For big, listed American companies the total has doubled, to about one-fifth. For Japanese firms it is about one-tenth, says Kathy Matsui of Goldman Sachs. The bigger a firm is, the greater its exposure tends to be. Rich-world firms do business across the emerging world, with China accounting for 10-20% of it. Consumer goods, cars, natural resources and technology are the industries with most exposure. Property, construction and health care have the least.

目前新兴市场面临的困难并没有1997-98年时那么糟糕。但是现在在新兴市场的发达国家的企业业务比当时多得多(见表2)。摩根士丹利的格雷厄姆塞克(Graham Secker)估算出大型欧洲企业的利润有三分之一来自发展中国家,这几乎是1997年水平的三倍。而对于美国大型上市企业来说,其在发展中国家的总利润已经翻番,大约占全部的五分之一。高盛公司的松井凯蒂表示日本企业在发展中国家的利润占总额的十分之一。企业规模越大,其对新兴市场的开放度越大。发达国家企业的业务遍布整个新兴市场国家,其中中国占10%-20%。消费品、汽车、天然资源以及技术产业在新兴市场的业务最多。而房地产、卫生保健的则最少。

Many of these operations pre-date the boom. European firms have footprints in Asia and Africa from colonial times. American firms dominated foreign direct investment (FDI) flows in the 1970s and 1980s. By the 1990s manufacturing firms were creating global production chains. A wave of privatisations in Latin America enticed a new generation of conquistadores from Iberia and North America. Many of these operations pre-date the boom. European firms have footprints in Asia and Africa from colonial times. American firms dominated foreign direct investment (FDI) flows in the 1970s and 1980s. By the 1990s manufacturing firms were creating global production chains. A wave of privatisations in Latin America enticed a new generation of conquistadores from Iberia and North America.

其中许多业务都开始于新兴市场繁荣之前。欧洲企业早在殖民时期就在亚洲和非洲留下了足迹。美国在20世纪70和80年代控制了外国直接投资。20世纪90年代制造型企业开始创建全球生产链。拉丁美洲的私有化浪潮吸引了来自伊比利亚半岛和北美的新一代征服者。

But by the mid-2000s the process had accelerated dramatically as executives and boards latched on to the idea of the fast-growing BRICs (Brazil, Russia, India, China) and their ilk. Once the subprime and euro crises began, the urge to escape the Western world was irresistible. FDI into China in 2010 was more than double the level in 1998. Takeovers became common. In 2007 purchases in emerging markets by rich-world firms reached $225 billion. That was five times the level just half a decade earlier. One measure of how discipline slipped is the valuation of those deals. In 2007 rich-world buyers stumped up a dizzy 17 times operating profits for their targets, double the multiple paid in 2000-03.

但是到2000年代中期,由于公司主管和董事们开始了解到金砖国家(包括巴西、俄罗斯、印度和中国)及其相似的国家经济发展迅猛,这一进程急速发展。次贷危机和欧债危机开始后,逃离西方国家就成为不可阻挡的潮流。2010年对中国的外国直接投资超过1998年时的两倍。收购成为普遍现象。2007年发达国家企业在新兴市场国家的收购额达到2250亿美元。这一数字是五年前的五倍。对这些交易进行估值可以看出限制减少了。2007年发达国家的买家掏出了其营业利润17倍的钱进行收购,这个数字是2000-03年间总额的两倍。

Some firms had unexpected identity changes. Suzuki, a Japanese carmaker, found that its formerly sleepy Indian arm accounted for the biggest chunk of its market value. Portugal Telecom’s Brazilian unit kept it afloat during the euro crisis. Having taken control of a beer firm in St Petersburg, Carlsberg, a Danish brewer, became a “Russia play”. Mandom, an 87-year-old Japanese firm, found itself a giant of the Indonesian male-cosmetics market.

没有预料到的是某些企业的定位发生了变化。日本汽车制造商铃木发现曾经无作为的印度分部现在已经成为其最大的市值来源。葡萄牙电信公司的巴西分公司在欧债危机期间仍保持运转。丹麦的啤酒制造商嘉士伯公司在收购了圣彼得堡的一家啤机公司后,成为了一个”俄罗斯企业“。有87年历史的日本企业漫丹发现自己已经成为了印尼男性化妆品市场的巨头。

Other firms’ efforts to peacock their emerging-market credentials look, with hindsight, like indicators of excess. Having been bailed out for its toxic credit exposures back in America, Citigroup rebranded itself as an emerging-market bank. Schneider Electric, a French engineering firm, and HSBC relocated their chief executives from Europe to Hong Kong (HSBC has since backtracked).

事后看来,其它公司努力想要炫耀其在新兴市场国家的资历似乎是这种现象过量的表现。在美国的坏账问题被解决后,花旗银行重新定位自己为发展中银行。法国工程企业施耐德电气和汇丰银行将其行政总部从欧洲搬到香港(汇丰属于原路折返)。

Historians may judge the peak of the frenzy to have been in June 2010. Nathaniel Rothschild, a scion of a banking dynasty (some of whose members are minority shareholders in The Economist), raised $1.1 billion for a shell company in London, set up to buy emerging-market mining assets. Months later it invested in Indonesian coal mines with the Bakrie family, known in that country for its political ties and web of businesses. According to Bloomberg, Mr Rothschild shook hands on the deal without visiting the main mine in question, in Borneo. The transaction was a “terrible mistake”, he later admitted.

历史学家或许会把这种疯狂行为的高峰定在2010年6月。纳撒尼尔罗斯柴尔德出身于一个银行业王朝(这个组织的某些成员是本刊的少数股东),他为一家伦敦的壳公司集资11亿美元,成立这家壳公司是为了购买新兴市场的矿业资产。几个月后这家壳公司与巴克利家族一同投资了印尼的煤矿,巴克利家族因其政治关系和商业网络在印尼很有名。据彭博社报道,罗斯柴尔德都没有参观过位于婆罗洲的这家煤矿就直接握手成交了。他后来承认这次交易是”巨大的错误“。

Every corporate-investment cycle creates triumphs and disasters, and a lot of mediocrity. The emerging-markets boom will be no exception. Hard figures are elusive but the book value of the equity that Western firms have invested in the emerging world has probably risen by at least $3 trillion since 1998. This is a colossal sum, equivalent to 11% of the emerging markets’ combined GDP in 2013. Many firms have prospered, such as the banks that braved Mexico in the 1990s. But there is plenty of rot, too.

每种企业投资循环都会有胜有败,也不乏平庸。新兴市场的繁荣现象也不会例外。虽然难以找到确切的数字,但是1998年以来西方企业在新兴市场的投资资本的账面价值至少上升了3万亿美元。这个数字极其庞大,大致相当于新兴市场国家2013年GDP的总和。许多企业都获得蓬勃发展,比如20世纪90年代顶住莫斯科危机的众多银行。但也有许多企业失败了。

Start with takeovers. There have been $1.6 trillion-worth since 2002. A rule of thumb is that half of all deals destroy value for the acquirer. Like Vodafone, many firms paid dizzy prices justified by pepped-up forecasts. In 2010 Abbott Laboratories, an American drugs firm, paid $4 billion for the small Indian drugs unit of Piramal, predicting it would grow at 20% a year for a decade. Two years later sales were stagnant in dollar terms. Daiichi Sankyo, a Japanese drugs firm, has been badly burned in India, as the company it bought into, Ranbaxy, has hit serious quality problems. Lafarge paid $15 billion for Orascom, a North African and Middle Eastern rival, in 2007. The French cement giant predicted sales would rise by 30% a year. Since then its shares have almost halved, partly due to the crippling debt burden incurred. Start with takeovers. There have been $1.6 trillion-worth since 2002. A rule of thumb is that half of all deals destroy value for the acquirer. Like Vodafone, many firms paid dizzy prices justified by pepped-up forecasts. In 2010 Abbott Laboratories, an American drugs firm, paid $4 billion for the small Indian drugs unit of Piramal, predicting it would grow at 20% a year for a decade. Two years later sales were stagnant in dollar terms. Daiichi Sankyo, a Japanese drugs firm, has been badly burned in India, as the company it bought into, Ranbaxy, has hit serious quality problems. Lafarge paid $15 billion for Orascom, a North African and Middle Eastern rival, in 2007. The French cement giant predicted sales would rise by 30% a year. Since then its shares have almost halved, partly due to the crippling debt burden incurred.

西方企业采取的第一步是收购。2002年以来收购值已达到了1.6万亿美元。粗略估计其中有一半的交易让收购者蒙受损失。比如沃达丰,听信许多夸大其实的预测,许多企业支付了足以让人晕眩的高价。2010年,美国雅培制药公司花了40亿美元买下皮拉马尔在印度的许多小型制药厂,估计未来十年的年均增值会在20%。两年后以美元计算其销售额陷入停滞。日本制药公司第一三共株式会社因其收购的印度南新公司面临严峻质量问题而损失惨重。2007年拉法基集团以150亿美元收购其北非和中亚的竞争对手奥斯康公司。这一法国水泥业大亨预测年均销售额会增长30%。但是从那时开始其股票几乎减半,部分是由巨大的债务负担引起的。

Big greenfield projects have broken hearts, too. ThyssenKrupp, a German steel colossus, launched an ambitious project in 2006 to make steel slabs in Brazil and process them in America. Rising costs have made it unviable, and most of the $10 billion sunk has been written off. The firm’s boss has labelled the episode a “disaster”. Anglo American, a mining company, buried $8 billion and the career of its former chief executive, Cynthia Carroll, in a Brazilian project called Minas-Rio. Cost overruns have led to a $4 billion write-off.

许多未实行的大项目也千疮百孔。德国钢铁大亨蒂森克虏伯2006年发起了一项宏伟的计划,在巴西制造钢铁板而在美国进行加工。但是不断增加的成本让这项计划难以成行,而已投入的100亿美元大部分也已冲销。该企业老板将称这次经历为“灾难”。矿产公司英美资源集团在巴西进行的名为米纳斯-里约的项目不仅葬送了80亿美元,也葬送了其前首席执行官辛西娅卡罗尔(Cynthia Carroll)的事业。开支不断增加导致40亿美元的账目被冲销。

Besides such eye-catching failures, there are pockets of serious underperformance tucked away in corners of sprawling multinationals. Consumer-goods firms have made hay in emerging markets, but even the best have some iffy businesses. Procter & Gamble’s margins outside America are half those it enjoys at home. Profits are weak in India and Brazil, where it is a laggard. A.G. Lafley, who returned as the firm’s boss last year, has promised more discipline.

除了这些引人注目的失败例子外,在众多的跨国公司中还有许多不为人知的表现不佳问题。许多消费品企业在新兴市场国家的利润渐微,即使是最好的企业也有一些问题。保洁公司在美国境外的利润是其在国内利润的一半,而在印度和巴西保洁由于经营不善,利润也很少。去年回归担任保洁公司领导人的A.G.拉弗里(A.G.Lafley)承诺会加强公司的纪律管理。

It is the same story with Spanish investments in Latin America. Telefónica makes good money across most of the continent, says Bosco Ojeda of UBS, a bank. But Mexico is a running sore. For 14 years Telefónica has poured in billions of dollars without threatening Carlos Slim, who dominates telecoms there. Even the world’s two biggest brewers, Anheuser-Busch InBev and SABMiller, which have been huge successes, have bought some businesses with low market shares and commensurately weaker profits and returns on capital.

西班牙在拉美的投资境况也是如此。瑞士联合银行的博斯科欧杰达(Bosco Ojeda)表示西班牙电信公司在欧洲大陆的绝大多数地区的利润都不错,但是墨西哥确实其软肋。14年来西班牙电信公司已投入了几十亿美元却没有动摇当地电信业霸主卡洛斯斯雷姆(Carlos Slim)的地位。即使是已获得巨大成功的世界上两家最大的啤酒制造商百威英博和南非米勒收购的企业的市场份额也很低,相应的利润和资本收益率也很低。

In some cases the underperformance is spread across an entire industry. During a boom every firm thinks it can be a winner, leading to excess investment and saturation. The more capital-intensive the industry is, the greater the pain in store for its weakest members. Insurance is a case in point. India has more than 20 foreign firms slugging it out for tiny market shares while bleeding cash. Turkey is also an insurers’ graveyard. Most European firms have a motley collection of emerging-market assets, but only a few, such as Prudential, AXA and Allianz, have scale. “There are trophy markets where everyone has decided they have to be in. Typically they don’t make a lot of money,” says an executive.

也有些表现不佳的问题是遍布于整个行业的。在繁荣时期每个企业都认为自己会是赢家,这种想法导致超额投资和饱和现象的出现。一个行业的资本密集度越大,其中的弱势企业未来蒙受的损失就会越大。保险业就是其中一个例子。印度有20多家外国企业一边不断投钱,一边相互争夺微小的市场份额。土耳其也是保险公司的坟墓。大多数欧洲企业拥有的新兴市场资产五花八门,只有包括保诚保险、安盛集团和安联集团的少数几家所拥有的新兴市场资产数额较大。一位执行官表示,“有很多盈利市场,每个人都觉得自己必须要进入其中。但是通常他们赚的钱并不多。”

The car industry also has a long tail of flaky businesses. It has invested more than $50 billion in factories in China, with great success, reckons Max Warburton, also of Bernstein. But “China has affected the judgment of a lot of chief executives,” making them too bullish about other emerging markets. More than $30 billion has been invested in developing countries other than China. New factories are opening just as demand has slowed. Ford’s number two, Mark Fields, this week expressed worries about excess carmaking capacity building up in Brazil, Russia and India. Mr Warburton thinks such operations could burn billions of dollars this year. “Everyone is bracing to lose a lot of money.”

汽车行业的失败生意也有很多。汽车行业在中国工厂的投资超过了500亿美元,麦克斯沃伯顿亦是麦克斯伯恩斯顿认为这项投资带来了巨大的成功。但是“中国影响了许多首席执行官的判断力,”让他们变得对其它新兴市场也信心十足,将300多亿美元的资金投在了中国之外的其它新兴市场国家。新工厂开业的同时市场需求也下降了。号称福特第二的马克菲尔兹本周对在巴西、俄罗斯和印度的汽车产业的过度建设表示了担忧。沃伯顿认为这种行为可能会造成今年的损失达到上百亿美元。“每个人都准备好了要损失很多钱。”

Taking the beer goggles off

冷静观察

Some rich-world firms need to take a long, cold look at their emerging-market businesses and work out if they make sense. But there are psychological barriers to this. One is that most Western businesses have low gearing—usually it is only when they have a debt problem that they make difficult decisions quickly. Without their emerging-markets pep pill many firms would have dire revenue growth. The developing world has supplied 60-90% of the growth of Europe’s big firms in recent years. And a whole generation of chief executives has learned that quitting emerging markets is a mug’s game. Bosses who panicked and left after the 1997-98 crisis ended up looking like idiots.

某些发达国家的企业需要采取长远、冷静的视角看待新兴市场的生意,并要研究其是否有意义。但是也存在这心理障碍。其中一点就是大多数西方企业的联动比率很低——通常情况下只有在有债务问题的时候他们才会迅速作出艰难的决策。没有心想市场这个兴奋药丸的话,许多企业的收入增长会极低。近些年来欧洲大型企业60%-90%的收入增长来自发展中国家。一整代首席执行官们都学到了放弃新兴市场的话等于把钱送了出去。那些在1997-98年危机中陷入恐慌并离开的老板们最后落得个傻瓜般的下场。

Yet companies should allocate capital carefully, regardless of the spare funds they have. Sales growth without profits is pointless. And comparisons with 1997-98 are imperfect. Most industries have become more competitive, as emerging economies’ local firms get into their stride. The low-hanging fruit is gone. Reflecting this logic, a few big industries have already begun to trim their emerging-markets arms.

但是无论有多少闲散资金,企业都应该谨慎分配资产。带不来利润的销售额增长是毫无意义的。与1997-98年的情况相比较也是有瑕疵的。随着众多新兴市场的本土企业加入,大多数行业的竞争变得更加激烈。唾手可得的果实已经吃不到了。有些大型企业开始削减其在新兴市场的分部门,这也是这一逻辑现象的表现。

Exhibit one is banking. After being bailed out, some firms such as ING and Royal Bank of Scotland have largely retreated from the developing world. Bank of America has sold out of its Chinese affiliate. But even big, successful firms which are dedicated to emerging economies are trying to boost returns by trimming back. HSBC has got out of 23 emerging-market businesses. The world’s biggest five mining firms are also adapting to lower emerging-market demand. They have cut capital investment by a quarter since 2012, says Myles Allsop of UBS.

其中一个例子就是银行业。包括荷兰国际集团、苏格兰皇家银行在内的某些企业在得到救助后,都撤离了发展中国家。美洲银行也出售了其中国的分公司。但那些规模更大更成功的致力于新兴经济体的企业正在试图通过削减部门来促进收益增长。汇丰银行已关闭了23家新兴市场的分部。世界五大矿业公司也在适应新兴市场需求不断减少的境况。瑞士联合银行的迈尔斯奥索普(Myles Allsop)表示,自2012年以来,这五家企业的资本投资额削减了四分之一。

The supermarkets are in retreat after decades of empire-building that led them to invest $50 billion in the emerging world. Synergies have proved elusive, local rivals have got stronger and tastes more particular. In Turkey shoppers prefer discount stores to hypermarkets—the four biggest foreign firms there lost money in 2012. Aside from Walmart’s Mexican unit, most rich-country grocers’ operations in the developing world have low market shares and do not cover their cost of capital. Casino, a French firm, has already shrunk, says Edouard Aubin, of Morgan Stanley. He thinks Carrefour could slim down to five countries from a peak of more than 20 (although it said this week it would keep expanding in China and Brazil). Walmart is cutting the number of stores it has in emerging markets. Tesco seems to have abandoned its dream of controlling big businesses in Turkey and China.

过去几十年在新兴市场国家投资了500亿美元以建立起一个庞大的帝国的超级市场现在也开始撤退。与其它企业合作的效果也不尽理想,本土竞争对手的实力越来越强、越来越与众不同。在土耳其由于消费者喜欢打折商店多于大型市场——2012年四家外国大型超市亏本。除了沃尔玛在墨西哥的分公司之外,大多数发达国家在发展中国家的零售业务的市场份额降低,并且面临亏本。摩根士丹利的埃杜阿德奥班(Edouard Aubin)表示法国企业卡西诺已经亏损。他认为家乐福可能会从高峰期20个国家减少至5个国家(虽然家乐福本周表示会继续扩展子中国和巴西的业务)。沃尔玛正在削减其在新兴市场的门店数量。而乐购似乎也放弃了想要控制土耳其和中国市场的梦想。

In the next few years more firms may follow the example of some supermarkets and retreat from the developing world. Most, though, will adapt, cutting capital investment and pruning their portfolios. All this will create opportunities for rising local firms. On February 19th, as Peugeot announced its giant write-off of emerging-market assets, Dongfeng, its Chinese partner, said it would take a 14% stake in the French firm and that technology-sharing between the two would speed up. There are rumours that General Motors may sell its loss-making Indian plant to its Chinese partner, SAIC. In 2011 ING sold its large Latin American business to Grupo Sura, a Colombian conglomerate intent on becoming a regional player.

未来几年会有更多的企业跟随这些超级市场的脚步撤离发展中国家。但是大多数会通过削减资本投资和业务来学着适应。这些都会为处于上升期的本土企业创造机会。2月19日,标致公司宣布大量冲销其新兴市场资产,其工作伙伴中国东风汽车公司表示会拥有标致公司14%的股权,而两家公司间的技术合作进程也会加快。有传言称通用汽车公司会将其亏本的印度工厂出售给其中国合作伙伴上汽集团。2011年荷兰国际集团将其在拉美的业务出售给哥伦比亚的苏拉集团,这家公司现在正致力于成为地区霸主。

The rich-world firms that remain will need to make their business models weatherproof, not just suited for the sunny days of a boom. That means shifting even more production to emerging markets and borrowing in local currencies—both are a natural hedge against currency turbulence.

继续留在新兴市场的发达国家企业将需要使其商业模式更加坚不可摧,而不是仅仅适用于繁荣的阳光时期。这就意味着要向新兴市场转移更多的生产业务,更多地借贷当地货币——这两种手段都应对货币动荡的天然屏障。

As others falter, the strongest multinationals are making bolt-on acquisitions. In 2013 Unilever bought out some minority shareholders in its Indian business for $3 billion and Anheuser-Busch InBev took control of Grupo Modelo, a Mexican rival, for $20 billion. The year before Nestlé spent $12 billion buying Pfizer’s baby-food business, which is mainly exposed to the emerging world. Rather than being the panacea envisioned by many Western firms during the boom, emerging markets are governed by the oldest business rule of all—survival of the fittest.

虽然它企业在衰落,但是实力最强大的跨国公司们却正在进行补强收购。2013年联合利华以30亿美元买断其印度分公司少数股东的全部股份,百威英博以200亿美元收购了其墨西哥竞争对手莫得罗集团。2012年雀巢以120亿美元收购了辉瑞公司的婴儿食品业务,这项业务主要面向新兴市场。新兴市场并不是许多西方企业在繁荣期所设想的万能药,它依然遵循最古老的的商业法则——适者生存。 |

豆瓣http://www.douban.com/people/knowcraft

博客http://www.yantan.cc/blog/?12226

微博http://weibo.com/1862276280 |

|